Physical Address

Crimson Lynx Media Ltd

Scottish Provident House

76-80 College Road

London

HA1 1BQ

Physical Address

Crimson Lynx Media Ltd

Scottish Provident House

76-80 College Road

London

HA1 1BQ

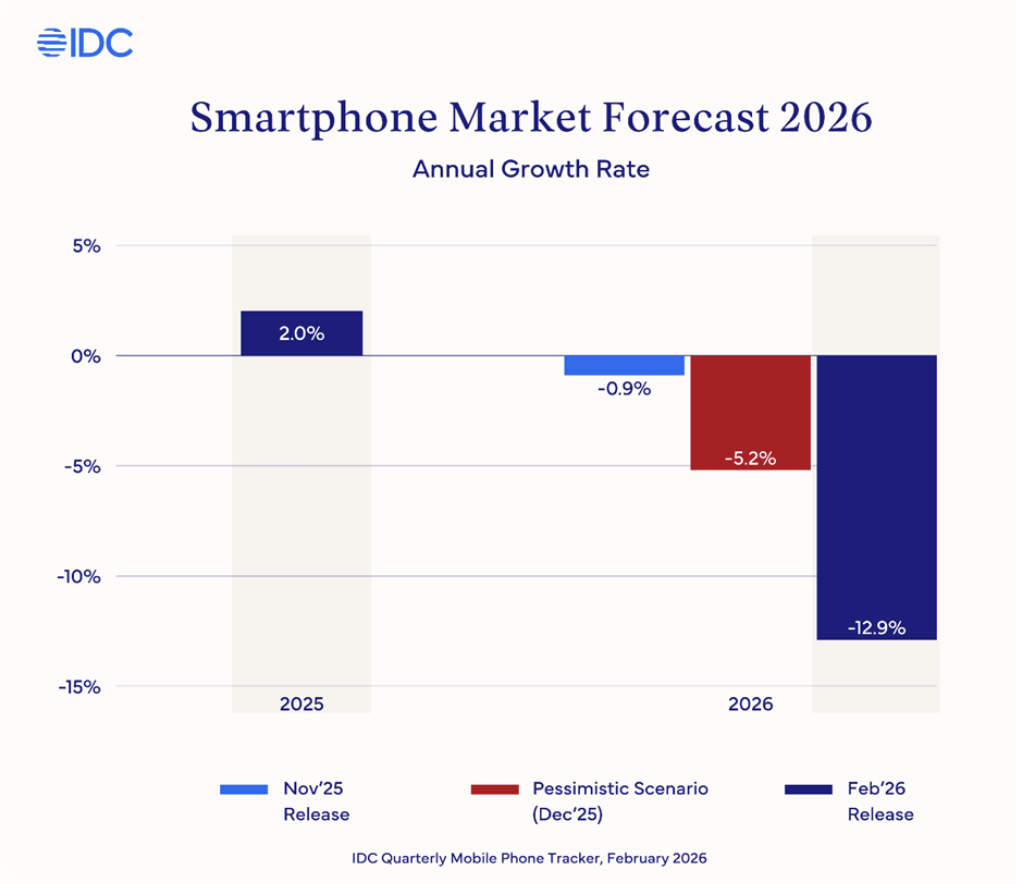

The global smartphone market faces a fresh wave of disruption

IDC has warned that a deepening memory shortage will persist through 2026 and likely into 2027, driving higher device prices, weaker specifications and a shift in market share toward the biggest brands.

“The “tsunami-like” shock has come to the consumer electronics industry, and the ripple effects will be felt by consumers and enterprises in the coming months” warns IDC VP Client Devices Francisco Jeronimo.

IDC says demand for DRAM and NAND from booming AI infrastructure is competing directly with consumer devices for limited supply, keeping prices elevated even as growth in memory costs begins to slow later this year. IDC does not expect prices to return to 2025 levels within its forecast horizon.

AI boom squeezing smartphones

The core problem is structural. Hyperscale data centres building out AI capacity are consuming huge volumes of memory, leaving PC and smartphone makers fighting over what remains.

Additional capacity from new fabs and smaller Chinese suppliers may ease the pressure slightly, but IDC says it will not be enough to change the overall trajectory.

Specs down, prices up

IDC expects some new smartphones to launch with lower memory configurations rather than absorbing rising component costs.

Devices that might have shipped last year with 12GB RAM and 256GB storage could now arrive with 8GB and 128GB at the same price point – or higher.

The pain will be most acute at the budget end of the market, where margins are already wafer-thin. IDC estimates more than 360 million smartphones shipped globally below $150 last year, representing a huge share of volumes in emerging markets.

That price band may become economically unsustainable.

Vendors focused on low-end devices are expected either to cut specifications sharply or push prices above $200, where demand is far weaker. Some may exit those tiers altogether.

Big brands to gain share

Companies with deeper pockets and stronger supplier relationships will be best placed to secure memory allocations.

IDC predicts meaningful share gains for the largest global OEMs in 2026, as smaller and regional players struggle to compete.

Knock-on effects could be significant:

Longer upgrade cycles as consumers delay purchases

Higher interest in refurbished and used smartphones

Reduced total addressable market in emerging economies

IDC says price-sensitive buyers may hold onto devices longer, turn to refurbished models or, in some cases, even revert to feature phones if ultra-low-cost smartphones disappear.

That trend could accelerate growth in the secondary market – a familiar theme for the circular mobile ecosystem many UK channel players are now targeting.

Tariffs add uncertainty

Trade policy is compounding the problem. IDC notes fresh US tariff proposals could add up to 15 percent to import costs on top of rising component prices, making pricing and sourcing decisions even harder for vendors and channel partners.

A structural reset ahead

IDC’s verdict is stark: the smartphone market is heading for a structural reset in size, product mix and competitive dynamics.

With memory shortages set to last well into 2027, vendors, distributors and can expect sustained turbulence.